Saving is the key to financial security. I know many people think saving is hard. However, when you see your account grow and compound over the years, it becomes exciting. You realize it wasn’t that hard, and saving actually gets easier over time. You just need to take the first step.

Thomas Stanley and William Danko, authors of “The Millionaire Next Door,” studied the traits of millionaires. They found that millionaires save at least 15 percent of their earned income and live well below their means. In addition, 80 percent did not receive an inheritance (they are self-made millionaires).

The authors coined the term “high-consumption lifestyle” to describe people who spend all their money, never save and never get wealthy. This describes many people, because there is constant pressure to overspend and keep up with the Joneses.

If wealthy feels out of reach, it should not. Many of my clients came from very poor backgrounds, but by saving throughout their working years, they became millionaires by age 55 or 60. Some of them are astonished when we discuss their net worth because they never expected to become millionaires. They exemplify the benefits of saving for the future.

If wealthy feels out of reach, it should not. Many of my clients came from very poor backgrounds, but by saving throughout their working years, they became millionaires by age 55 or 60. Some of them are astonished when we discuss their net worth because they never expected to become millionaires. They exemplify the benefits of saving for the future.

Saving is powerful; the trick is to make it automatic. If you have a retirement plan at work (such as a 401(k) or 403(b)), contribute to it. The contributions automatically come out of your paycheck before you are paid, and you will not miss them. Many employers “match” a part of the employee’s contribution, and you should never pass this up. Therefore, if your employer provides a match, make sure you contribute enough to earn the full match. If you have questions, go to your benefits office and ask them to help you set it up.

Next, you should know how much you are contributing to the retirement plan. Is it 5 percent? Bump it up to 8 percent. If it is 10 percent, consider bumping it up to 12 percent. Aim to save at least 15 percent of your earned income.

Next, you should know how much you are contributing to the retirement plan. Is it 5 percent? Bump it up to 8 percent. If it is 10 percent, consider bumping it up to 12 percent. Aim to save at least 15 percent of your earned income.

Where else can you save? A savings account at your local bank or credit union is perfect for an emergency fund. If you don’t have a savings account I recommend you open one. Tell the person helping you at the bank or credit union that you want a savings account that will not have any fees. I suggest building this fund to the level where it can cover six months of expenses in case of an emergency.

A Roth IRA is another excellent choice. My February article will cover details about Roth IRAs, but for now, just know that a Roth IRA is a high priority because the money you invest in it will grow tax-free. As long as a person has earned income, a person under age 50 can contribute $5,500 to a Roth and someone who is 50 or over can contribute up to $6,500. (Earned income must be at least $5,500 or $6,500 to contribute the full amount.) You can contribute to a Roth IRA until April 18, 2017, for the 2016 tax year, and you can contribute again for the 2017 tax year (between Jan. 1, 2017, and April 16, 2018).

Perhaps you are thinking “How can I save? I need every penny for my monthly expenses.” This is where you need to get creative. Clearly, you must pay the rent or the mortgage, and many expenses are “fixed.”

However, buying groceries, eating out and entertainment are not fixed expenses. They are “discretionary,” meaning you have control over them.

With groceries, consider not buying soda for the next month. How about not buying sweets? If you eat out three times a week, reduce it to twice a week. Perhaps you like new clothing or shoes, and you buy items on impulse. Try not buying new clothing for the next three months.

From all these possibilities, calculate how much you can realistically save each month. It will likely add up to $50-$100 per month, but it may be even higher. Set up automatic savings so your bank or credit union will sweep the amount you choose into your savings account at the beginning of each month. You will quickly adjust to having slightly less cash available – and you’ll be on your way to saving.

There are other ways to save for the future. One way to kick your savings into high gear is to save at least one half of your tax refund. Likewise, if you get a 4 percent raise, plan to save at least 2 percent and you can spend the remaining 2 percent.

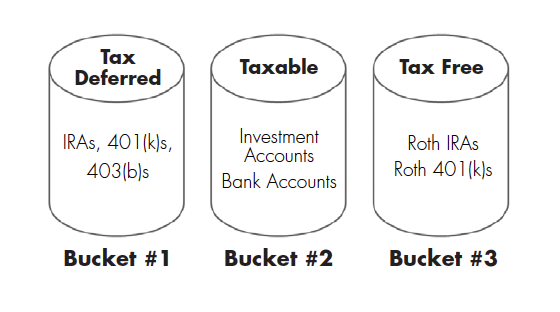

Part of the power of savings is from compounding. Keeping an emergency fund in a savings account will not compound because most banks and credit unions do not offer interest on these accounts. (That’s acceptable because the savings account should be only for emergencies.) Money saved in your 401(k) or 403(b) will compound with the earnings each year. Saving in a Roth IRA, a traditional IRA, or a taxable investment account will also compound.

The “Rule of 72” tells us that if your investments earn 7.2 percent (on average) per year, the investments will double in value every 10 years. This rule explains the power of compounding, but it only pertains to the return on your investment. It does not include additional contributions during the 10 years. It is the additional contributions each year (plus the power of compounding) that causes investment accounts to grow very rapidly.

Let’s look at the result of consistent saving and compounding. At left is a chart that shows the impact of saving $200 per month, $500 per month, or $1,000 per month. An average annual return on the investment account of 6 percent is used. This is a conservative assumption for a balanced investment account consisting of 50 percent Vanguard 500 Index fund and 50 percent Vanguard Total Bond Market Index fund. (This would be called a 50 percent equity and 50 percent fixed income portfolio). The historical average annual return for this portfolio was approximately 8.26 percent (per year) for the past five years, 5.82 percent for the past 10 years, 5.45 percent for the past 15 years, 6.36 percent for the past 20 years, and 8.47 percent for the past 30 years. (Historical data is from Morningstar.)

The two Vanguard funds used in this example have very low expenses, and it is assumed that dividends, interest and capital gains will be reinvested. The chart shows the impact of saving and compounding over 10, 20 and 30 years. Keep in mind the values in the chart are only estimates, because you will not experience exactly 6 percent return each year on your investment account. Your actual returns will be lower – or higher – than the returns shown.