ALBUQUERQUE, N.M. — Many people are intimidated by money. They don’t know where to begin to get organized. Some people may work with a financial adviser and not be directly involved in managing their money. Other people do not know what they own and whether their net worth is a positive or negative number.

Putting your head in the sand does not make it better, and I strongly recommend that everyone take control of their money. Creating a net worth statement is a great place to start. It is easy and quick, and it will help you decide where to focus your attention for improving your financial future.

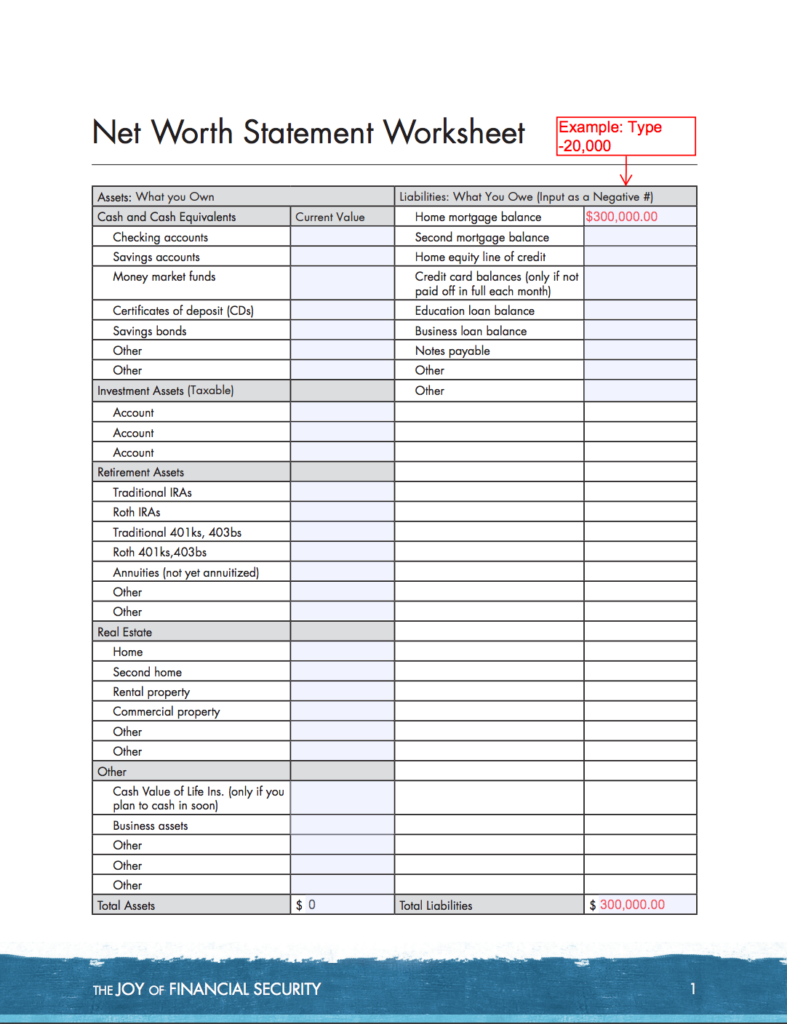

A net worth statement worksheet is provided, and it is simply a list of your assets (what you own) minus your liabilities (what you owe). If you prefer to work online, find it at joyoffinancialsecurity.com/ net-worth/.

You probably received a year-end statement for any investment or bank accounts you own, so begin by gathering the statements into one pile so you can easily find what you need.

First, list your assets. This includes checking and savings accounts, CDs, investment accounts (including retirement accounts, such as IRAs, Roth IRAs, taxable accounts, 401(k), etc.). Next, list your home and other real estate you own. Estimate what you think your home may be worth.

First, list your assets. This includes checking and savings accounts, CDs, investment accounts (including retirement accounts, such as IRAs, Roth IRAs, taxable accounts, 401(k), etc.). Next, list your home and other real estate you own. Estimate what you think your home may be worth.

Do not list pensions or Social Security benefits. These are income streams, but they do not belong on your list of assets. I also recommend you do not include cars, jewelry or artwork. Typically, these items are not going to be sold, so they should not be considered assets.

Next, list your liabilities. This includes the balance on your mortgage, and any other debts such as car loans, credit card balances that are not paid in full each month, and college loans.

Total the asset and the liabilities at the bottom of each column. Subtract the liabilities from the assets, and the result is your current net worth.

What’s next? I encourage you to update it each year. You will see improvement, but it will not be linear. If you are saving in your 401(k) through your employer, you will see that balance increase. If you are saving in a taxable account or funding a Roth IRA, you will see those values increase. If you have credit card debt, I encourage you to commit to paying it off quickly.

Your net worth may increase by 10 percent or 15 percent one year, but it may decrease in another year. The performance of the stock and bond markets will impact your net worth if you have investment accounts, but other factors you control – such as savings, funding a Roth IRA or your retirement accounts at work, paying off credit card balances or car loans – will have a greater impact. If you pay off your credit cards or a car loan, put that money (that previously went toward your monthly payment) into your saving each month.

Once you complete your net worth statement, congratulate yourself! You have taken a huge step forward in improving your financial security.